Let’s start with an easy question. What is the Individual Coverage Health Reimbursement Arrangement (ICHRA)?

ICHRA is an innovative health benefit that allows employers to reimburse employees for their health insurance premiums and other qualified medical expenses. This arrangement differs from traditional employer-sponsored coverage because it enables businesses to maintain cost control while fulfilling the Minimal Essential Coverage (MEC) requirements.

More health plans are exploring opportunities to offer tailored support to employees who opt for Marketplace coverage funded by an ICHRA. As health plans evaluate the potential benefits of integrating ICHRA into their services, a few questions keep appearing.

1. How Is ICHRA Different from Employer-Sponsored Coverage?

ICHRA is gaining traction with employers and employees as group premiums rise, and the need for affordable alternatives grows. If ICHRA is better for employers and employees, it inherently benefits the health plan by expanding coverage options to those who may be priced out or ineligible for employer-sponsored or government-subsidized coverage.

Why Employers and Employees are Opting for ICHRA:

Flexibility and Customization: In 2020, 74% of firms only offered one type of health plan to employees. ICHRA allows employers to reimburse employees for individual plans that best meet their personal and family health care needs. This autonomy enables employees to select plans that provide optimal coverage, leading to happy members.

Cost Control: Employers can establish defined contribution limits, which affords them greater control over their health insurance budgets. This level of predictability aids businesses in planning without the unpredictability of premium spikes common with group plans.

Reduced Risk: By allowing employees to manage their own health coverage, employers mitigate the risk, shifting the responsibility of health management to the employees.

Provider Flexibility: Employees enjoy the freedom to choose health plans that include their preferred doctors and health care providers, ensuring that their health care aligns with their expectations and needs.

Plan Portability: ICHRA benefits are portable and remain with employees if they change jobs, offering continuity that is not typically available with traditional employer-based plans.

Tax Advantages: ICHRA offers notable tax benefits. Employers enjoy tax deductions on contributions, while employees benefit from tax-free reimbursements.

Compliance and Simplicity: From an administrative perspective, ICHRA plans are less complex to manage than traditional group plans. This simplicity is particularly beneficial for small businesses, reducing their administrative load and ensuring compliance with fewer burdens.

ICHRA offers an opportunity for health plans to adapt to a changing market, especially as they seek to transition high-risk groups to more sustainable models like the ACA Marketplace.

Benefits of ICHRA for Health Plans:

Enhancing Member Retention: Stability is a significant benefit of ICHRA. Even if employees lose their jobs, the transition from ICHRA funds to Advanced Premium Tax Credits (APTCs), can help members maintain their coverage without disruption. This continuity is especially valuable in maintaining long-term relationships with members, providing them with a sense of security and trust in their health plan.

Simplifying Administration: Since ICHRAs are used to purchase QHPs, health plans do not need to design ICHRA-specific plans. This can be an administrative relief for health plans consistently needing to design plans to fit the needs of group purchasers.

Easy Payment Processes: Employees utilizing ICHRA are typically not duel-eligible for APTCs. Additionally, ICHRA Administrators are responsible for taking employer-provided funds and applying them as requested, paying all or a portion of the employee’s premiums. This simplifies the payment process for health plans, as they do not have to integrate with multiple funding sources when payments are made through the ICHRA Administrator.

Role of Brokers

One thing remains the same between the coverage types, the importance of the broker. Brokers continue to play a crucial role in advising employers on the best health coverage strategies for their businesses, assisting with the setup and management of ICHRA plans, and ensuring that employees understand their benefits and how to use them effectively.

2.What are People Saying About ICHRA’s Future?

ICHRA is not just a passing trend. First introduced in June 2019 by the Trump administration, ICHRA expands the benefits of Qualified Small Employer Health Reimbursement Arrangements (QSEHRAs) to businesses of all sizes.

Continued Growth: ICHRA usage is climbing as more employers adopt and renew HRAs.

Large Employer Adoption: There’s exponential growth in large employers choosing ICHRA solutions.

Nationwide Adoption: Hundreds of thousands of U.S. workers across all states now receive ICHRA or QSEHRA as a benefit.

Market Impact: ICHRA and QSEHRA are increasingly serving as gateways for adding new lives to the ACA Marketplace.

Since its introduction in 2020, ICHRA has seen nearly 350% growth, with the U.S. Department of Labor projecting an additional 255% growth by 2025. This significant increase primarily occurred over the past two years, following a slow adoption in its first year.

The year-over-year growth from 2023 to 2024 neared 30%, with Applicable Large Employers (ALEs) being the fastest-growing segment.

Given the rising enrollments in both ICHRA and ACA, along with the increasing costs of traditional group marketing, there’s a strong economic incentive for businesses to adopt ICHRA.

3. What Individuals are Most Likely to Enroll in an ICHRA Plan?

Individuals with Limited Access to Employer-Sponsored Coverage

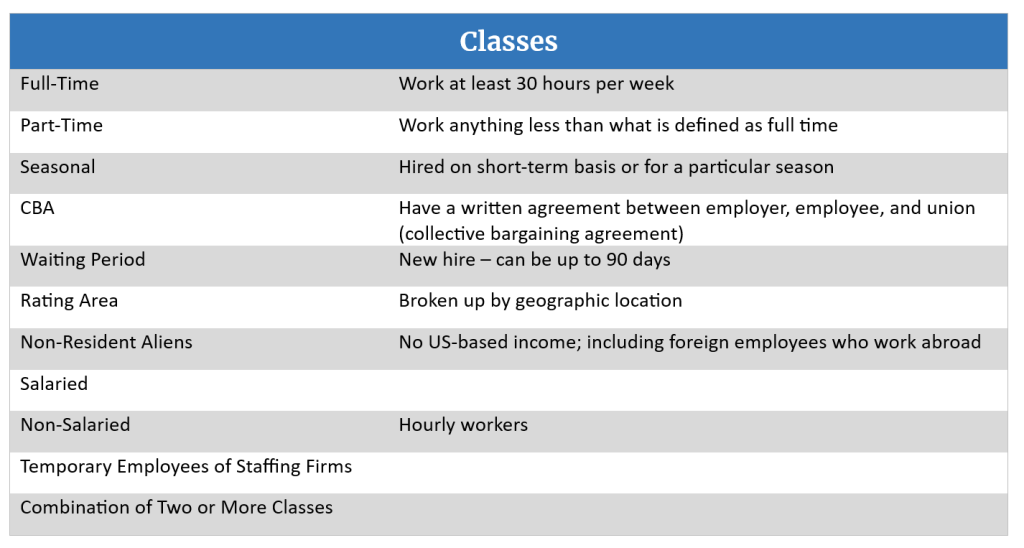

ICHRA is specifically designed for employees who lack traditional employer-sponsored coverage options, focusing on meeting the needs of the underinsured. Employers can categorize their workforce into 11 different ICHRA classes, including groups traditionally underserved by employer health plans:

Under ICHRA guidelines, employers must ensure fair distribution of funds contributions within each class; employers can provide up to three times more funding to the oldest employees compared to the youngest. Cover can extend to employee’s spouse and dependents, with adjustments in contributions based on family size. This flexible class structure enables ICHRA to extend coverage to employees who previously lacked employer-sponsored options.

Traditionally, younger generations have either been overlooked by employer-sponsored plans or priced out of subsidized coverage. To effectively cater to these often geographically dispersed members, health plans need to prioritize a strong provider network capable of supporting remote employees.

4. What Does the ICHRA Administration Look Like?

With ICHRA, the pressure is taking off the health and placed on the employers for making sure the correct administrative processes are in. But that doesn’t mean health plans can’t help. Designing QHPs that meet the needs of local workers, supplementing member communication, and providing a personalized shopping experience are just some of the ways health plans can support employers offering ICHRA.

While each employer will create their own specific process, here’s an ICHRA administration workflow:

Configuration: This initial step involves setting up the ICHRA plan according to the employer’s specific needs and preferences. This includes selecting the appropriate software or platform to administer the ICHRA.

Define Classes: There are 11 employee class for employers to categorize their employees. Employees can be broken out based on job roles, locations, full-time or part-time status, etc.

Define Contributions: The employer determines a fixed dollar amount to contribute towards each class. This amount can vary across each employee class, with age and family status being variable factors.

Employee Roster: A comprehensive list of employees participating in an ICHRA for each class type is prepared and uploaded accordingly to the platform chosen. This roster includes all relevant details needed to administer the benefits for each employee, including name, date of birth, class, and contribution amount.

Review Affordability: When offering an ICHRA, it must meet the affordability criteria set by the ACA. Employers will need to ensure their ICHRA contributions meet this requirement to avoid penalties and ensure compliance. Reliable and trusted platforms should have safeguards in place that will check that affordability requirements are met.

Notify Employees: With contributions determined, classes defined, and affordability calculations met, employees are then informed about their ICHRA offerings and how to utilize the benefits should they opt in. This notification often includes guidance on how to shop for and enroll in a qualified plan.

Shop & Enroll: Once notified of their ICHRA plan and contribution amounts, employees can use the funds to shop for and enroll in a qualified health insurance plan. This step is critical and relies solely on the employee. If they do not purchase a qualified plan, they are not eligible to be reimbursed with the ICHRA funds and will not have health coverage.

Submit Receipt: After a plan is purchased, employees will submit receipts for reimbursement on the premiums and any QMEs. Each employer determines their own reimbursement process. Regardless of how reimbursements are handled, employees will need to maintain proper documentation for all medical expenditures.

Reimburse Expenses: All submitted expenses will be reviewed by the employer’s designated benefits administrator and once approved, the employee will be reimbursed per the employer’s predetermined process.

Maintenance: Regular maintenance of ICHRA plans involve ongoing administrative tasks such as updating employee information and ensuring compliance with regulatory changes.

5. How Does ICHRA Couple with Federally Facilitated Marketplace and State-Based Marketplace Policies?

ICHRAs can reimburse coverage purchased both On and Off-Exchange in all 50 states. However, federal-subsidized premiums available through the Federally Facilitated Marketplace (FFM) and State-Based Marketplaces (SBMs) cannot be combined with the funds provided through an ICHRA. This stipulation may create challenges for individuals in accessing affordable health insurance options.

Given the income thresholds for qualifying for subsidized coverage through the Marketplace, it’s anticipated that most employees with ICHRA would not be eligible for zero to low-cost Marketplace plans. This tradeoff highlights a significant consideration for health plans as they assess the role of ICHRA within their coverage offerings, especially in terms of member affordability and plan accessibility.

6. How Can Health Plans Integrate ICHRA Into Their Offerings?

Health plans interested in integrating ICHRA face several operational and technical considerations. Strategies for inclusion within a broader product portfolio need careful planning, especially for health plans witnessing declines in traditional employer-sponsored profit margins or those looking to expand their ACA business.

Offer a Tailored Shopping Experience for ICHRA

A pivotal component in supporting ICHRA is offering a tailored shopping experience that aligns with the health plan’s existing enrollment processes. This could include a “one-stop branded shop” for consumers using their ICHRA benefits, complete with recommended insurance plans and estimated out-of-pocket costs factoring in ICHRA contributions. The improvements and enhancements that have been effective in growing ACA enrollments should be adapted and applied to optimize the ICHRA shopping experience.

Building a Support Network

Beyond technical integration, successful adoption of ICHRA by health plans also depends heavily on building and maintaining strong partnerships with BenTech agencies and brokers. These relationships are crucial as they help navigate the complex landscape of health insurance, ensuring that the ICHRA offerings are not only compliant but also competitive and well-positioned within the market. Effective collaboration with these stakeholders is essential to maximize the reach and impact of ICHRA plans, facilitating better outcomes for all.