Turn Rising Premiums into Member-Retention & Growth with ICHRA

Give future members and their employers a flexible, tax-advantaged health benefit while you lock in loyalty, reduce churn, and open a new acquisition channel.

ACA premiums are climbing, and members are looking for more affordable ways to stay covered. Every lost member impacts reputation, revenue, and growth. That’s why national and local health plans are investing in ICHRA to:

Build Lifelong Loyalty

Give members a reason to stay for life, not just for a plan year. ICHRA lets employees keep their preferred carrier as their jobs, income, or subsidies change. Softheon keeps every transition connected through one consistent member experience.

Drive Off-Exchange Enrollments

Turn employer contributions into Off-Exchange growth. The ICHRA Connector Cloud routes eligible employees to your plans, helping you capture new membership and avoid costly CMS fees.

Keep Admin Costs Low

Our all-in-one, API‑first solution goes live in weeks, with built‑in compliance, reporting, and member‑experience tools, expanding your plans reach.

Futureproof your Individual and Group Strategy

As ACA premiums skyrocket, ICHRA positions your plan as the flexible, member‑centric option that the market demands. Industry-leading plans have already started.

Trusted by Health Plans and Their Members Nationwide

“Anyone in group coverage knows the prices are rising. And they are rising astronomically. Small employers are cutting it off and deciding to not offer more and more every year… With ICHRA, we now have an opportunity to use our Marketplace plans and, through ICHRA administration with Softheon, offer smaller employers a more affordable healthcare option.”

Daverick Isaac | Community First Health Plans

“For small businesses, offering health insurance essentially requires them to run their own insurance company alongside their core business. Health plans have a real opportunity to take that burden off their plate while making healthcare more affordable, accessible, and plentiful.”

Eugene Sayan, Founder, President, and CEO of Softheon; Chairman of the HRA Council

No noise – Just actions. Our free guide breaks down some of the misconceptions around ICHRA and provides the know-how for your plan to effectively compete in the ICHRA market.

The Key to ICHRA Growth: Softheon’s Connector Cloud

Eliminate Unnecessary CMS Admin Fees

Our data show that 13% of all On‑Exchange members receive a $0 subsidy, yet carriers are still paying the mandatory 2.5 % CMS administrative fee for those lives. Most of these members are ICHRA‑eligible employees of small employers that do not offer traditional group coverage. By routing these individuals through Softheon’s ICHRA Connector, carriers can remove those dead‑weight fees and provide a more affordable, compliant health‑coverage option to the employee.

Clear, Conflict‑Free Roles – Softheon Is the Agent of Record, Not the Broker

Softheon never assumes the Broker‑of‑Record (BOR) function. We operate strictly as the Agent of Record (AOR) for the health plan, preserving the plan’s fiduciary control and preventing the conflict‑of‑interest alerts that CMS flags when a single entity claims both broker and agent status.

One Integration, Unlimited Distribution

With the ICHRA Connector, health plans can exponentially expand their access get access to any number of brokers through with just a single integration. This single‑point‑of‑entry model eliminates duplicate integrations, reduces IT overhead, and accelerates time‑to‑market for ICHRA offerings.

Unified, End‑to‑End Member Experience Across All Lines of Business

ICHRA is just one piece of your plan’s portfolio. Softheon’s multi‑market architecture consolidates Marketplace, ICHRA, and Medicare Advantage on one platform. Members enjoy a single, seamless journey — from initial enrollment (“cradle”) through every transition (“grave”) — while carriers benefit from a unified data view, consistent member communications, and streamlined operations.

Get a Jump Start on ICHRA Growth & Enrollment with these Helpful Resources

ICHRA RFP Guide for Health Plans

Preparing Your Health Plan for ICHRA Growth? Start with the Right RFP

What Makes Softheon an Ideal ICHRA Growth Partner?

Softheon is already well-established in helping Payers expand their ACA business into ICHRA. We have the trusted connections to Third-Party Administrators (TPAs) including ICHRA Administrators and other Benefit Technology providers that expand your plan’s reach while maintaining ICHRA compliance. Let us fast-track your ICHRA go-to-market efforts.

For health plans interested in adding ICHRA to their coverage offerings, here are a few reasons why we excel as a potential partner:

What do payers need to launch and scale ICHRA programs?

To participate in ICHRA, health plans need systems that support employer-class definitions, contribution settings, affordability checks, and member-facing shopping tied to reimbursement logic. Softheon already connects enrollment and billing flows to ICHRA/third-party administrators via API or EDI.

By automating reconciliation of employer contributions and premium payments plans can scale ICHRA without manual admin burden or costly errors. One added benefit: Plans can attract employers and employees migrating out of traditional group coverage.

ICHRA

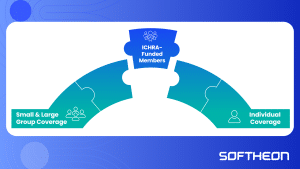

How do health plans handle ICHRA plus Marketplace interactions?

ICHRA funds cannot combine with Marketplace subsidies (yet!), so plans must keep Off-Exchange and On-Exchange experiences separate but aligned. Softheon’s system creates clear enrollment pathways for both, maintaining compliance and regulatory requirements.

This lets plans attract ICHRA members without disrupting existing ACA operations.

ICHRA

What are the advantages of ICHRA-funded plans vs. traditional group plans?

ICHRAs give employers more control and flexibility than traditional group coverage while still offering employees access to high-quality plans. Key advantages include:

Cost control: Group premiums typically rise about 5% per year. With ICHRA, employers set their own contribution amounts and budgets.

Flexibility by class: Employers can offer different reimbursement amounts across eligible employee classes without breaking compliance rules.

No participation requirements: Unlike group plans, ICHRA does not require a minimum percentage of employees to enroll, supporting organizations with distributed or variable workforces.

This structure helps employers stabilize benefits spend and stay competitive while directing more employees into ACA-compliant individual coverage.

ICHRA

What does the enrollment experience look like for employees?

Once employers finalize their classes and roster, employees receive a secure, personalized link to begin shopping. Their information is pre-populated to avoid redundant data entry, and a guided shopping flow supports plan selection. After choosing a plan, employees can submit their binder payment without any redirects.

ICHRA

How does Softheon manage premium payments and administration?

Softheon supports payment handling based on the plan’s preference, either direct to the carrier or through Softheon’s integrated billing engine. Members pay their binder and ongoing premiums in one place, and the system automates invoicing, processing, and reconciliation with CMS. With more than 20 years of billing and payment experience including Exchange operations, we streamline the flow to reduce member friction and improve retention.