The Affordable Care Act (ACA) is once again undergoing major policy and operational changes. In early July 2025, Congress advanced the One Big Beautiful Bill Act (OBBBA) alongside a newly finalized CMS rule — the Marketplace Integrity and Affordability Rule — bringing sweeping updates to Marketplace eligibility, enrollment timing, and verification processes.

These changes will impact Marketplace coverage, Medicaid transitions, and the systems payers and partners rely on to stay compliant. At Softheon, we’re breaking down what this means for your operations and how to prepare.

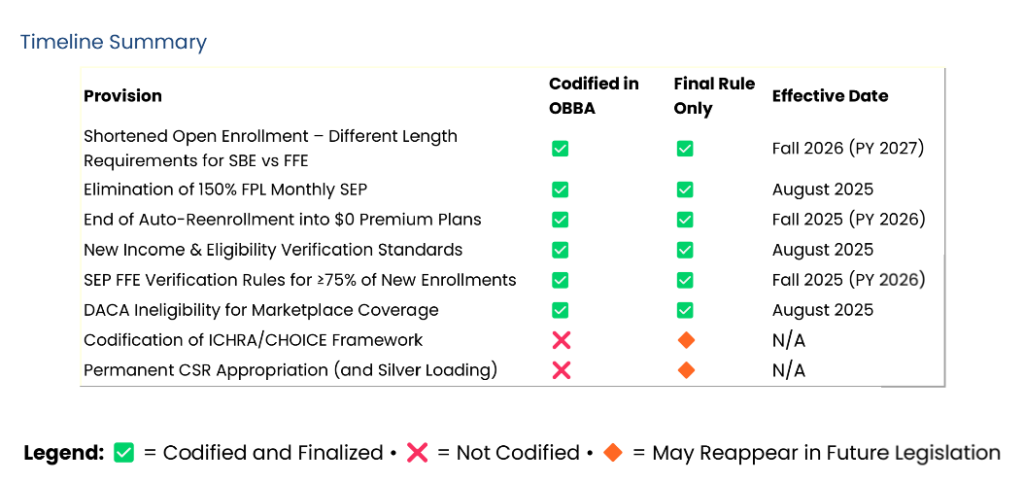

OBBBA Has Passed — But Not Everything Made It In

OBBBA (H.R.1, 119th Congress) has passed both chambers of Congress, with the House set to vote again on Senate revisions before final reconciliation. While the legislation includes several impactful policy shifts, not all originally proposed items made it into the final bill.

ICHRA/CHOICE Codification Was Removed

Although the House version of OBBBA included provisions to codify Individual Coverage HRAs (ICHRA) under the new name Custom Health Option and Individual Care Expense (CHOICE) arrangements, those sections were removed from the Senate-passed bill due to procedural rules. As a result, ICHRA remains governed by regulation, not statute, and no new expansion has taken place at this time.

However, speculation in Washington suggests that a separate bipartisan “health extenders” package may be introduced later this year. That bill could revisit ICHRA codification alongside potential updates to premium subsidy structures and CHOICE-related guidance.

CSR Appropriations Also Left Out

Similarly, the proposed federal appropriation of cost-sharing reduction (CSR) payments — which would have ended the practice of silver loading — was excluded from the final version. As a result, silver loading remains in place, with benchmark premiums and Advanced Premium Tax Credit (APTC) amounts continuing to reflect this structure.

Marketplace Changes That Will Directly Affect Health Plans

The new rules and legislation introduce multiple updates that will significantly impact how health plans engage with enrollees, process applications, and manage renewals. Below is a breakdown of the most consequential operational changes.

Shorter Open Enrollment Period Starting for Plan Year 2027

Beginning in fall 2026 (for coverage effective in 2027), the annual Open Enrollment (OE) on HealthCare.gov and most State-Based Marketplaces (SBMs) will be shortened. The current window of November 1 through January 15 will change to November 1 through December 15.

This move is intended to accelerate plan selections, limit prolonged unpaid effectuation windows, and reduce churn caused by passive enrollments. All SBMs will be required to adhere to this change, with no enrollment period extending past December 31.

Note: This does not affect the upcoming fall 2025 enrollment cycle (for Plan Year 2026), which will still run through January 15, 2026.

Elimination of the Low-Income Special Enrollment Period (SEP)

Starting in August 2025, the ongoing Special Enrollment Period (SEP) for consumers earning less than 150% of the Federal Poverty Level (FPL) will be eliminated. This SEP allowed eligible consumers to enroll year-round — and its removal will reduce continuous enrollment flexibility for many low-income households.

End of Automatic Re-Enrollment for Subsidized Members

Significant changes are coming to passive renewal logic:

For Plan Year 2026, enrollees in plans that would have automatically renewed with a $0 net premium will now be required to pay at least $5 per month, unless they take active steps to confirm eligibility. The goal is to ensure that consumers regularly update application data rather than drifting through year-over-year auto-renewals.

For Plan Year 2027, the legislation calls for the complete elimination of automatic re-enrollment for all subsidy-eligible members. This means that unless consumers actively renew, they will not retain coverage — even if eligible.

These changes will require updates to renewal notices, passive renewal workflows, and outreach campaigns to prevent unnecessary coverage loss.

Stricter Verification Requirements for Income and SEP Eligibility

Beginning in August 2025, multiple verification policy updates will take effect, including:

The 60-day grace period for resolving income inconsistencies will be removed. All inconsistencies must now be addressed within 90 days, in alignment with the statutory timeline.

Consumers who attest to income above 100% FPL will be required to submit documentation if trusted data sources indicate income below that threshold.

Consumers will also be required to submit income documentation if IRS tax data is unavailable for eligibility confirmation.

Additionally, beginning with Plan Year 2026, HealthCare.gov and participating platforms must obtain documentation for at least 75% of SEP enrollments, a significant increase in verification burden for plans and technology vendors alike.

DACA Recipients Will Lose Marketplace Eligibility

As of August 2025, recipients of the Deferred Action for Childhood Arrivals (DACA) program will no longer be eligible for ACA Marketplace coverage or premium subsidies. This reverses a previous policy update and will require prompt eligibility logic updates, training refreshers, and outreach to immigrant-serving organizations.

How Softheon Supports ACA Plans Through Regulatory Shifts

These policy changes are not just regulatory updates — they are operational challenges that will impact your enrollment timelines, member retention, and technology stack.

At Softheon, we’ve supported more than 100 licensed carriers with ACA Marketplace enrollment, billing, reconciliation, and compliance for nearly two decades. We’re here to help you:

Reconfigure eligibility and enrollment logic across On- and Off-Exchange systems

Update notices, SEP workflows, and passive renewal processes

Improve data accuracy and readiness for increased verification requirements

Ensure a unified member experience as coverage transitions become more complex

Whether you’re operating on an SBM, are a provider-sponsored plan, or ACA carrier looking to future-proof your operations, our platform adapts with the regulatory landscape — so you can stay focused on serving your members.