What Health Plans Need to Tackle in the next 365 days.

Author: Brandon Redman, VP of Healthcare Solutions at Softheon

Key takeaways:

- Aetna’s exit impacts 1M+ members across 17 states — a major opportunity for regional and provider-sponsored plans to step in.

- Plans that scaled successfully during Bright’s exit had flexible infrastructure, broker readiness, and automated reconciliation.

- Community plans must act now to retain market share, align internal ops, and prepare for a potential surge in ACA enrollees.

Another national carrier has stepped back from the ACA Marketplace. This time, it’s Aetna.

Like everyone else, my first thought was: “Oh, crap. This is going to cause some waves.” And it will.

If that sounds familiar, it should. We’ve seen this movie before. When Bright Health made its abrupt exit in 2023, hundreds of thousands of members were left scrambling for new coverage — and health plans rose to the scalability challenge or got crushed by it. In states where plans were prepared, enrollment skyrocketed. Some saw membership jumps of over 9,000% compared to the prior open enrollment period.

Ironically, one of the biggest winners from Bright’s exit? Aetna.

Aetna’s withdrawal will affect over a million members across 17 states. And if the Bright exit taught us anything, it’s this: Confused members don’t wait around for perfect answers. They move — fast — and they follow the path of least resistance. That creates a massive opportunity for health plans. But only if they’re ready to catch the membership wave before it crashes.

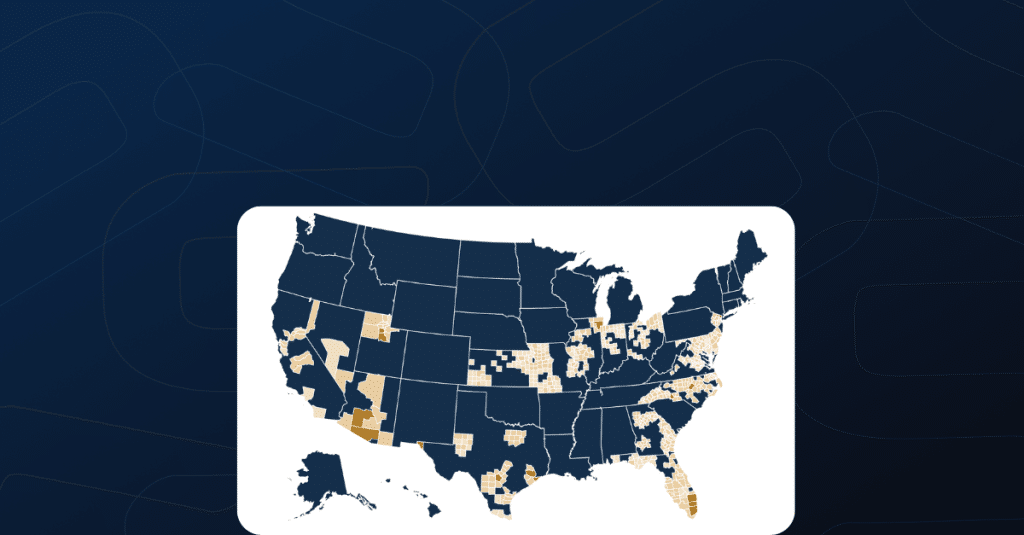

Aetna’s ACA Marketplace Footprint

*Created using Mark Farrah Associates’ data, based on county-level health plan enrollment figures.

Don’t Expect New Giants — But Do Expect Movement

Let’s be realistic: We’re not expecting a new wave of national health plan entrants to take Aetna’s place. Large carriers are staying cautious. But for smaller and regional plans? This is a moment of opportunity to make targeted, strategic moves.

We’re already seeing success stories from payviders (provider-sponsored) and community health plans stepping up to fill coverage gaps in their local markets. Take Baylor Scott & White (BSW), for example. They left the ACA market in 2016 due to poor performance — but reentered following the Bright Health exit and quickly captured a sizable portion of the individual market in Texas.

And what about local health systems that may see this as their moment to enter the ACA space? I’m especially curious about Banner Health. Aetna and Banner currently operate a joint venture that combines Banner’s integrated care teams and care-management capabilities with Aetna’s health plan experience. But with Aetna exiting the ACA, Banner may find itself without its plan counterpart.

In a recent interview with HealthLeaders Media, Mark Gavin, SVP of Partnerships and Venture Development at Banner, shared that Banner is looking to go beyond traditional healthcare models. “Why wait for someone else to come to the table?” he asked. “Why not be part of the creation, either [as] an owner or a partner or in a joint venture?”

The challenges? Many plans are already stretched thin. Acquisition budgets are tight. Talent is limited. And the pressure to do more with less keeps growing. Add to that the headwinds in the individual market — like the expected expiration of enhanced subsidies at the end of the year and historically limited marketing funds for the ACA under the Trump administration — there are big hills to climb on the trail to success.

But that doesn’t mean community members don’t need Individual market options. If anything, the need is growing.

Build Flexibility Before the Floodgates Open

Most health plans weren’t ready for Bright’s abrupt departure. And many still aren’t ready for the next major shakeup — like Aetna’s exit.

When enrollment data starts flowing from the Federally Facilitated Marketplace (FFM), State-Based Marketplaces (SBMs), direct enrollment partners, and third-party brokers, it can overwhelm systems that rely on manual processes or outdated architecture.

Plans that stayed ahead of the curve had already invested in flexible, modular systems that could:

- Automatically ingest and sort 834 enrollment files, regardless of the source

- Normalize and map data to a consistent structure for use across billing, reconciliation, and communication tools

- Process high volumes of member data in real time, without bottlenecks or manual cleanup

In moments of volatility, flexibility isn’t just about moving faster. It’s about being able to respond when the market shifts — and say “yes” when others can’t.

From Enrollment to Retention: What High-Performing Plans Got Right

Winning new members is only half the equation — keeping them is where the real work begins.

During the Bright Health exit, the plans that succeeded didn’t just show up with marketing campaigns. They showed up with a guided experience from the first outreach through plan selection and onboarding.

Here’s what separated the top performers:

- Educated brokers drive growth: For many plans, over half of all ACA enrollments come through brokers — and their role is only expanding with the rise of ICHRA as a flexible alternative to traditional employer-sponsored coverage. The most successful plans didn’t just activate broker networks; they educated them. That meant offering early appointments, localized assignments, and co-branded digital tools, but also training on everything the plan had to offer, including ICHRA-enabled individual coverage options. When brokers understand the full range of current and future offerings, they’re better equipped to guide employers and members alike — and more likely to bring those members to your doorstep.

- Digital-first onboarding: Rather than forcing new members into a call center bottleneck, high-performing plans offered intuitive shopping and enrollment experiences with built-in decision support. That approach helped drive faster plan selections and reduce drop-off.

- Operational readiness behind the scenes: Fast, accurate reconciliation between enrollment, payment, and eligibility data was critical. Plans that had automation in place kept their effectuation rates high — even when dealing with member surges.

None of this required reinventing the wheel. But it did require systems and teams that were ready to scale. Plans that waited for third-party notices or hesitated to staff up their broker support lost out.

The lesson? Members follow clarity. Brokers follow readiness. And retention follows both.

Final Take: Zig When the Market Zags

Half the battle in ACA is knowing when to move. Bright Health’s exit was a warning shot. Aetna’s is confirmation: Market volatility is the new normal.

Plans that succeed will be the ones that are ready — not reactive. Right now, plans in counties with high Aetna enrollments are focused on first understanding these members. By drilling down into demographics, health needs, and subsidy profiles, they can anticipate how these shifts will impact risk pools.

Then comes preparing for the needs of this new membership. That means aligning operations, brokers, and member communication tools around solutions, people, and processes that don’t break under pressure. The question is no longer if your plan will face a member influx. It’s when. And how ready you’ll be when it happens.

Let us help you get ready. If you have any questions about how your community-focused or provider-sponsored plan should be preparing for Aetna’s exit, find me on LinkedIn or schedule some time to talk here.