A Q&A for Health Plans with Commercial, Marketplace, and ASO Lines of Business

June 2026 | By Eugene Sayan

Key takeaways for health plans:

- ICHRA is creating new growth opportunities rather than simply replacing traditional group coverage.

- Health plans can leverage existing Marketplace, commercial, and ASO capabilities to support employers through multiple funding models.

- Consumer experience, operational excellence, and care management will become increasingly important competitive differentiators.

- Plans that prepare for ICHRA today will be better positioned to capture future membership growth.

Recent criticism of Individual Coverage Health Reimbursement Arrangements (ICHRAs) argues that employers should think carefully before replacing traditional group health plans with defined-contribution models.

That’s a reasonable discussion. However, many of these arguments are viewed exclusively through the lens of employers.

Health plans should ask a different question:

What if ICHRA is not a disruption to employer-sponsored healthcare, but the next growth engine for health plans?

Just as 401(k)s transformed retirement while creating entirely new markets for financial services firms, ICHRA is creating new opportunities for carriers, provider-sponsored health plans, and organizations with Administrative Services Only (ASO) business that are prepared to lead.

Let’s explore some of the most common questions.

Q: If employers move toward ICHRA, doesn’t that threaten traditional group business?

A: Not necessarily.

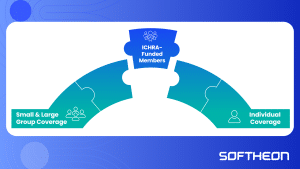

Many health plans view ICHRA as a migration away from group coverage. A more accurate perspective is that ICHRA creates a bridge between the group and Individual markets.

Today, many health plans already operate multiple lines of business, including commercial group, the Individual ACA Marketplace, Medicare Advantage, Medicaid, and ASO services.

ICHRA allows health plans to serve employers through a different funding mechanism while retaining membership, provider relationships, care management programs, and operational infrastructure. The employer remains the sponsor. The health plan remains the insurer. And the difference is how coverage is funded and selected.

Q: Critics argue that ICHRA does not solve healthcare inflation. Why should health plans care?

A: Because health plans understand that controlling costs requires engagement, data, and care management, not simply a different funding mechanism.

ICHRA does not solve healthcare inflation. Neither did traditional group plans. What ICHRA does create is a more consumer-driven environment where health plans compete on:

- Member experience

- Provider access

- Care management outcomes

- Digital engagement

- Quality ratings

- Value-based care performance

Plans that consistently deliver measurable value will be better positioned to attract and retain members, while those that rely primarily on employer purchasing decisions may face increasing competitive pressure. The future will reward consumer-centric health plans.

Q: Doesn’t ICHRA create adverse selection risk for health plans?

A: Only if health plans choose not to participate.

Every major shift in healthcare financing raises questions about risk selection. The ACA Marketplace, Medicare Advantage, and employer self-funding all faced these same concerns.

The organizations that succeeded invested early and learned how to manage risk effectively. Health plans already possess sophisticated capabilities in:

- Risk adjustment

- Population health management

- Predictive analytics

- Member engagement

- Provider network optimization

Those capabilities position health plans to thrive in an expanding ICHRA ecosystem.

Q: Why should health plans embrace ICHRA if they already have a successful employer group business?

A: Because employers are demanding greater flexibility.

Employers want more predictable healthcare budgets, reduced administrative burden, multi-state workforce flexibility, simplified compliance, and personalized employee experiences.

The question is not whether employers want these capabilities. The question is who will provide them. Health plans that offer both traditional group coverage and ICHRA solutions can meet employers wherever they are in their journey. Those that don’t may eventually lose market share to more adaptable competitors.

Q: How does ICHRA help plans with existing ACA Marketplace products?

A: This may be one of the biggest growth opportunities in healthcare.

The opportunity isn’t hypothetical. According to the HRA Council’s 2025 Growth Trends Report, adoption among applicable large employers (50+ employees) increased 34% year over year, while adoption among small employers grew 52%.

Many health plans have invested heavily in Marketplace products, consumer engagement platforms, enrollment infrastructure, digital shopping experiences, and broker channels.

Historically, employers and the individual market operated separately. ICHRA creates a bridge between them.

83% of employers offering an ICHRA or Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) in 2025 had not previously offered health coverage. That means ICHRA is often expanding access to coverage rather than simply shifting members from one product to another.

Employers become a new source of membership growth for Marketplace products, while health plans gain access to employer-sponsored premium dollars by leveraging existing Marketplace investments.

This creates a powerful flywheel:

- More employers drive more members

- More members improve scale

- Greater scale supports network expansion and product innovation

- Better products attract more employers

Q: What about health plans that provide Administrative Services Only (ASO)?

A: ICHRA may represent an even larger opportunity. Many health plans already provide ASO services, including:

- Eligibility management

- Enrollment administration

- Billing

- Premium collection

- Compliance support

- Employer reporting

- Member communications

These operational capabilities translate naturally to ICHRA administration. As employer adoption grows, organizations will increasingly need support with:

- Contribution management

- Employee shopping experiences

- Carrier connectivity

- Premium aggregation

- Reconciliation

- Compliance automation

Health plans with established ASO operations already have much of the infrastructure needed to deliver these services at scale.

Q: Is ICHRA replacing employer-sponsored healthcare?

A: No. ICHRA is modernizing employer-sponsored healthcare.

- Employers still fund healthcare

- Health plans still provide coverage

- Employees gain greater choice

- The market gains greater flexibility

This evolution mirrors what happened in retirement benefits. The shift from pensions to 401(k)s did not eliminate employer-sponsored retirement. It transformed how employers and employees shared responsibility. Healthcare is beginning a similar transition.

Q: What should health plans do now?

A: Start preparing before demand outpaces your operational readiness.

Many health plans already have the pieces in place. They offer commercial products, participate in the Individual market, support employer groups, and in many cases provide ASO services. The opportunity isn’t to build something entirely new. It’s to connect those capabilities into a strategy that supports employers, brokers, and members as ICHRA adoption grows.

That means thinking beyond product offerings. It means asking whether your enrollment, billing, payments, member engagement, and reporting infrastructure can support a more connected, consumer-driven model.

The health plans that start planning today will be in a much stronger position than those waiting for the market to mature.

The Future of ICHRA Starts Now

ICHRA shouldn’t be viewed as a threat to employer-sponsored healthcare. It represents another way for health plans to grow, strengthen employer relationships, and compete in an evolving market.

The organizations that will benefit most aren’t necessarily the first to enter the market. They’ll be the ones with the operational foundation to support employers and members at scale.

If your organization is evaluating its ICHRA strategy, now is the time to identify where your existing capabilities create an advantage and where operational gaps may limit future growth.

Schedule a conversation with our team to discuss your ICHRA strategy and see how leading health plans are preparing for the next phase of employer-sponsored coverage.